The primary sukuk market expanded significantly in 2025, benefiting from supportive global financing conditions.

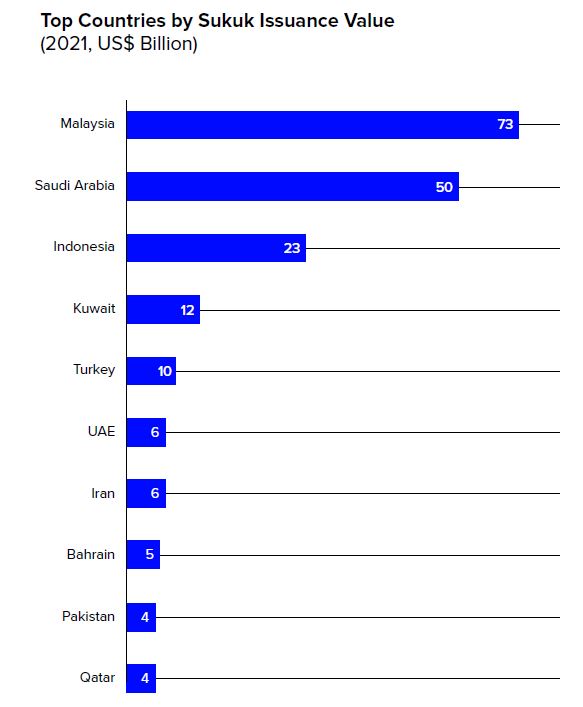

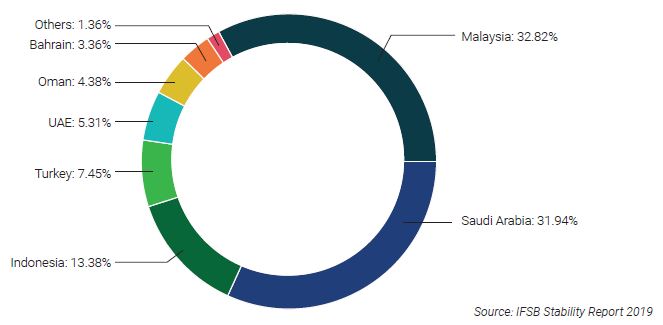

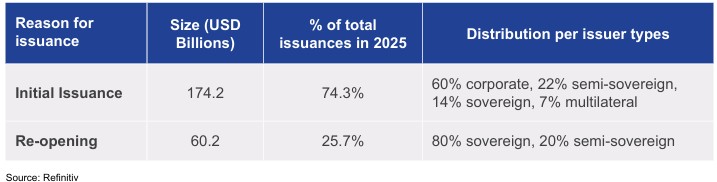

Total issuance’s climbed to USD 234.5 billion, with Malaysia and Saudi Arabia accounting for the majority of new offerings. Despite this robust issuance activity, market development has remained uneven across jurisdictions. In many countries, sovereign and quasi-sovereign entities continue to dominate the issuance landscape, while corporate issuers, although becoming more active, participate only intermittently, constraining broader market expansion.

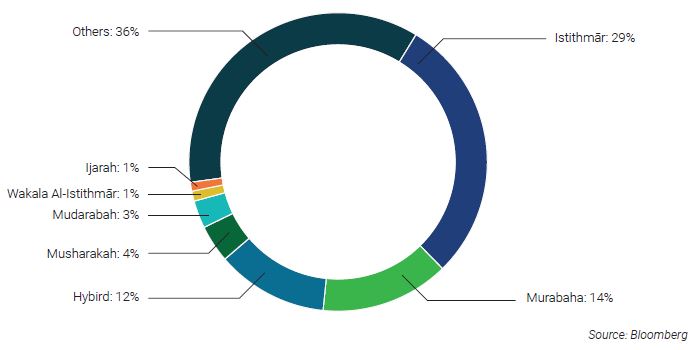

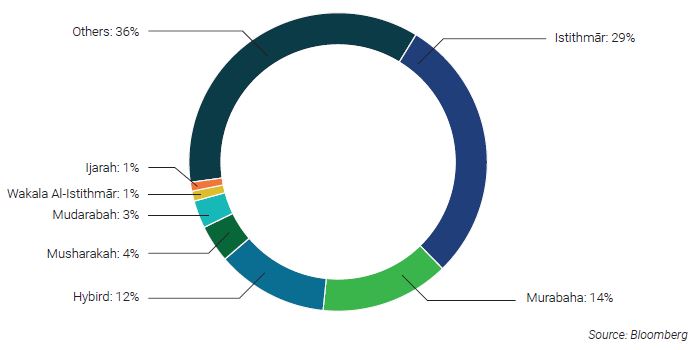

Moreover, a substantial proportion of ṣukūk issuance’s continues to be structured as one-off transactions, with relatively few reopening existing issues, particularly in the corporate segment. Consequently, despite record issuance volumes, the market remains fragmented. This fragmentation reduces fungibility, weakens secondary market liquidity, and limits the efficiency of price discovery

Source: IFSB

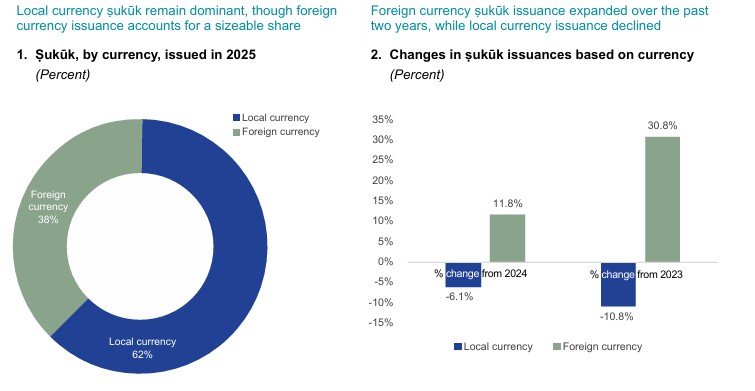

Domestic ṣukūk issuance declined for a second consecutive year, while activity in international markets strengthened, highlighting persistent weaknesses in local currency capital markets alongside increasingly favorable global funding conditions. Although local currency-denominated ṣukūk continue to account for a substantial proportion of total issuance, the overall funding mix has shifted between 2023 and 2025, with domestic issuance losing momentum as foreign currency issuance gained prominence.

local currency-denominated ṣukūk continue to account for a substantial proportion of total issuance

The increased reliance on international funding reflects both cyclical and structural factors. Improved global liquidity, lower external funding costs, and sustained investor demand for ṣukūk have encouraged issuers to access offshore markets. At the same time, limited market depth and constrained institutional investor capacity in several domestic markets have reduced the ability of local markets to accommodate larger financing requirements. While greater access to international capital markets enhances funding diversification, it also increases exposure to exchange rate risk and cross-border capital flow volatility, potentially strengthening the transmission of external financial shocks to domestic markets.

In several jurisdictions, the expansion of sovereign ṣukūk issuance has also reinforced the role of domestic Islamic banks as the primary investors in local currency issuances. This concentration reflects the relatively narrow domestic investor base and the continued dependence on captive investors, particularly banking institutions, to absorb sovereign financing needs. Such a structure may create financial stability vulnerabilities by increasing the interconnectedness between sovereign balance sheets and the banking sector, while also limiting the availability of financing for private sector borrowers.

Where sovereign exposures represent a significant share of Islamic banking assets, the sovereign-bank nexus remains an important source of systemic risk. In the event of sovereign debt stress or restructuring, concentrated holdings of government ṣukūk could generate sizeable balance sheet losses for Islamic banks and amplify risks to the wider financial system. Consequently, rapid growth in ṣukūk issuance does not necessarily imply stronger market resilience. Without broader institutional investor participation and deeper domestic capital markets, elevated issuance volumes may continue to coexist with underlying structural weaknesses and heightened financial stability risks.